45% CAGR from Copper Pureplay | Sandfire Resources (ASX:SFR)

Sandfire Resources: the copper miner that kept performing

April 2026 Update

Sandfire Resources has performed well beyond the expectations of the original model. If an investor did purchase the stock in July 2022 for $4.38, they would have tripled there money (2.96x). Over 3.7 years that is a 45% CAGR!!!.

The lesson is to revisit old ideas. Never know when they will continue to perform over the long term. I personally sold when I was happy with the return.

Preface

This is a historical analysis from 29 July 2022. One of the earlier stock notes.

Disclosure: I purchased SFR in my personal portfolio post the analysis and then sold the position at a 20% profit in 2022.

Valuation Summary

Executive Summary

Sandfire Resources Ltd (SFR) is a Perth-based copper mining company. It operates mines in Australia, Botswana, and Spain. Copper dominates SFR’s production, it is 82% of the total production. SFR is being recommended as a BUY with a price target of $6.47 from its current price of $4.38.

A simple discounted free cash flow to firm model was employed. It also includes a FCF margin exit multiple matrix as a scenario analysis. The price target represents a 47.72% gain as of July 28, 2022. The expectation is that demand for copper will increase globally for the energy transition and as China reopens fully as the largest consumer of raw materials.

Investment Thesis

Crucial Metal: Copper is a versatile metal. It is used as a conductor of electricity for TV’s, electric cars, battery storage, wiring, air conditioners, circuit boards, and mobile phones (to name a few). Copper is used in the smelting of brass; it does not corrode easily and is malleability enough for water piping. All these factors make copper a vital material for the foreseeable future.

Supply Demand Gap: According to major exchange copper inventory data (LME, Shanghai Copper, COMEX), copper inventories were at their height in Q1 2018 and have slowly been reducing overtime. Demand appears to be greater than the supply and it will take time for the companies to mine copper into a state for refinement. There are a few large companies in Australia that mine copper, and various other materials (BHP, OZL, NCM). There is enough of a gap in the market for Sandfire Resources to fill the increasing demand.

Expand Operations: Per the recent (and timely) results presentation, Sandfire Resources has a few mines in operation with more exploration activity underway. Sandfire’s Motheo mine is being constructed on schedule with the Definitive Feasibility Study (DFS) nearing completion, due for release in September 2022.

Market Trends

Copper is seen as a proxy for economic activity, lower copper prices generally indicate a weaker economy. This has been the case at the moment and copper prices have decreased since June as a result of economic fears.

Central banks have been aggressively increasing policy rates to curb inflation. This has the risk of potentially pushing economies into recession; less economic activity, less need for new construction, lower employment etc…

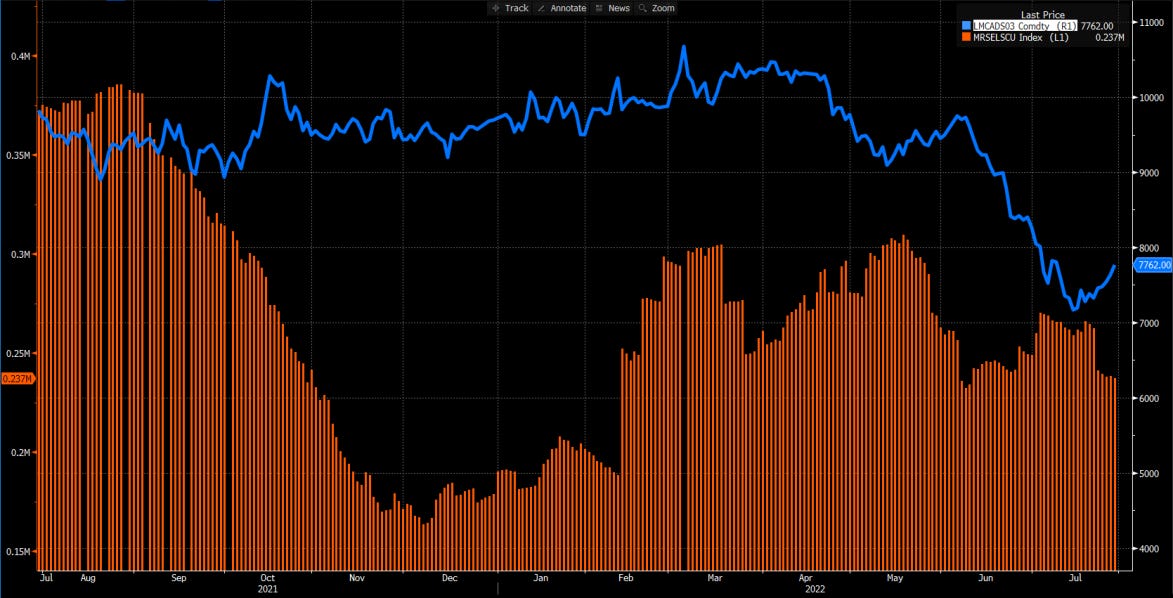

Copper being an element with many applications has dropped in price as short- term demand reduced. Below is the LME Commodity price of copper (Blue) compared to the major exchange copper inventory data (from LME, Shanghai Copper, and COMEX) (Orange).

Source: Bloomberg

ESG Analysis

Being a miner that digs ore from the ground is a tough starting point from an ESG perspective. Sandfire Resources has made some commitments to being sustainable and published a sustainability report in 2021.

Environmental

Sandfire has joined an association to reduce water consumption and developed tools to manage water catchment and usage. They are making efforts to reduce their water consumption, but mining tends to be a water heavy industry. The MATSA Mining Water Living Lab Project commenced in 2021 with the aim to promote the recovery and reuse of water in the mining industry. The pilot plant is taking place in the Aguas Teñidas Mine facilities. Sandfire have also been increasing their usage of solar energy, but this is a fraction of their overall energy consumption.

Social

Sandfire provided its first Early Childhood Sponsorship for children in Botswana. The sponsorship supports disadvantaged children within the Ghanzi district to obtain educational opportunities. Sandfire have a number of social initiatives in the pipeline to promote the workforce and engage with communities in the areas they operate. According to Bloomberg, this area of ESG is where Sandfire is most lagging behind.

Governance

Board and senior management are a good mix of men and women. As stated in their report, Sandfire regularly reviews its governance practices and policies to reflect current legislation and best practices. Remuneration of the board and management has incentives for performance and with a combination of cash and share options.

Risks

There are a number of risks to consider with this investment. Sandfire’s revenue mostly comes from copper sales. As mentioned before, negative sentiment usually leads to lower copper prices. Also, if the world is hit with another COVID variant the company’s operations will be impacted and delay construction of the Motheo mine. If inflation remains persistent, central banks may continue to increase interest rates beyond expectations. This will increase costs of floating rate debt and will most likely reduce the interest coverage ratio of Sandfire. I recently accumulate debt for the new mines.

Valuation

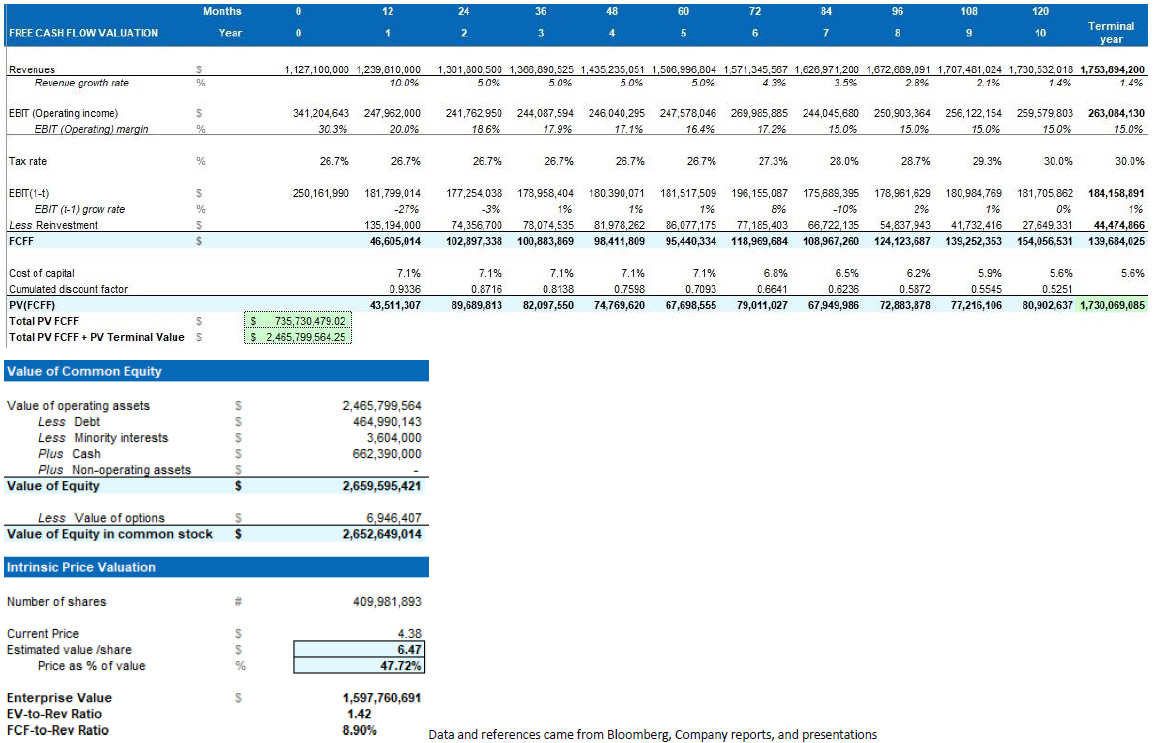

Using last years’ financial report, Bloomberg, and the most recent quarterly update as at July 2022, I’ve modelled an FCFF valuation with a margin matrix. Given time available I used a simple and conservative approach. FCFF was reached from via EBIT less any reinvestment.

The reinvestment amount was based off the sales to capital ratio which was calculated to be 0.83 (Sales/( BV of Equity + BV of Debt less Cash). WACC was calculated as 7.11%. Using a risk-free rate of 1.35% (RBA cash rate) and country Equity Risk Premiums based on weighted revenues.

Part of the FCFF valuation output is the FCF to Sales margin (8.90%). The model calculated an average 10-year revenue growth rate of 4.38%. This was based on the initial assumptions and the output of the model.

Again, I wanted to be conversative and this (in my mind) made up for the fact that commodities are cyclical. Sandfire itself has seen swings in the EBIT margin and revenue growth. The share price valuation based on my model was $6.47.

Target Price Matrix

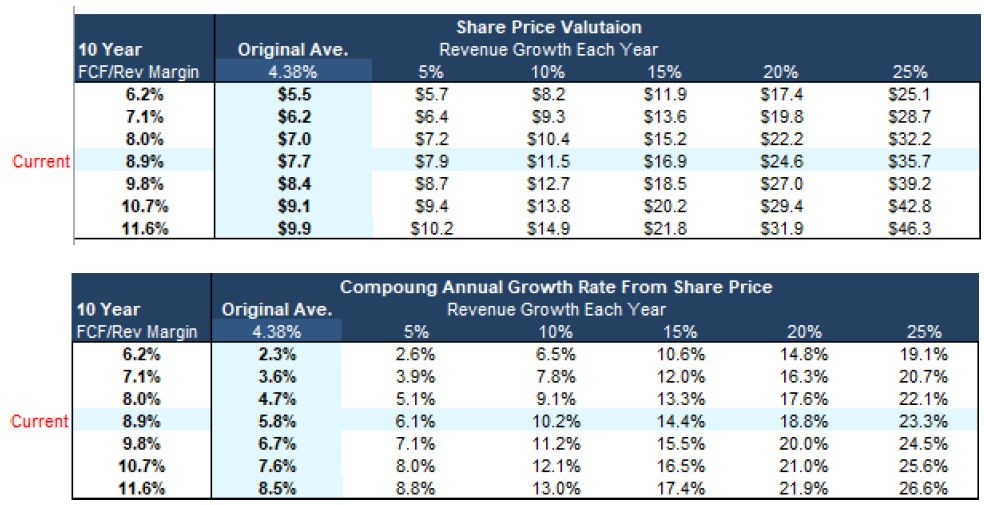

Assuming other 10-year revenue growth rates, I produced a matrix of share prices and CAGR. When looking at the tables below, it gives an idea of what the share price could be if the long run revenue growth and FCF margin changes.

So, a $6.47 per share valuation is at the lower end of the matrix. Considering the current share price is near its COVID lows, there is plenty of potential upside before it reaches its previous 12M high of $7.43 per share.

Disclaimer: Content is for educational purposes only and does not constitute financial advice. Always do your own research.