8% Yielding Global Infra Exposure for 10 years - Atlas Arteria (ASX:ALX)

Alternative Toll-Road player to Transurban

Preface

This is a historical analysis from January 2026.

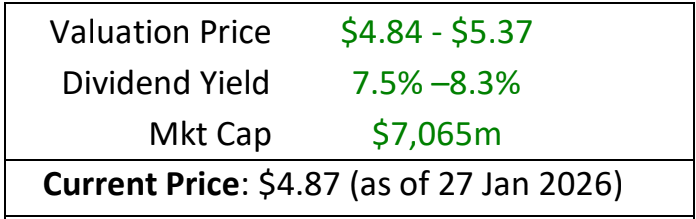

Valuation Summary

Executive Summary

Atlas Arteria (ALX) is a global owner and operator of toll road networks, with its primary value derived from its stake in the APRR motorway group in eastern France. ALX was valued at a price range of $4.84 - $5.37 (base to middle case) using a Dividend Discount Model. The stock serves as an attractive income play, offering AUD-hedged distributions with a yield of 7.5% - 8.3%. This investment thesis remains valid through to 2035, the year the concession for its most significant asset is scheduled to expire.

Investment Thesis

ALX provides Australian investors with exposure to high-quality foreign infrastructure assets while hedging currency risk for the distributions. The portfolio benefits from long-dated concession lives and robust pricing power. While the APRR agreement concludes in 2035, the remaining assets benefit from concession structures that allow for toll increases linked to CPI or specific flat-rate rises. This provides a reliable, steady revenue backed by essential infrastructure.

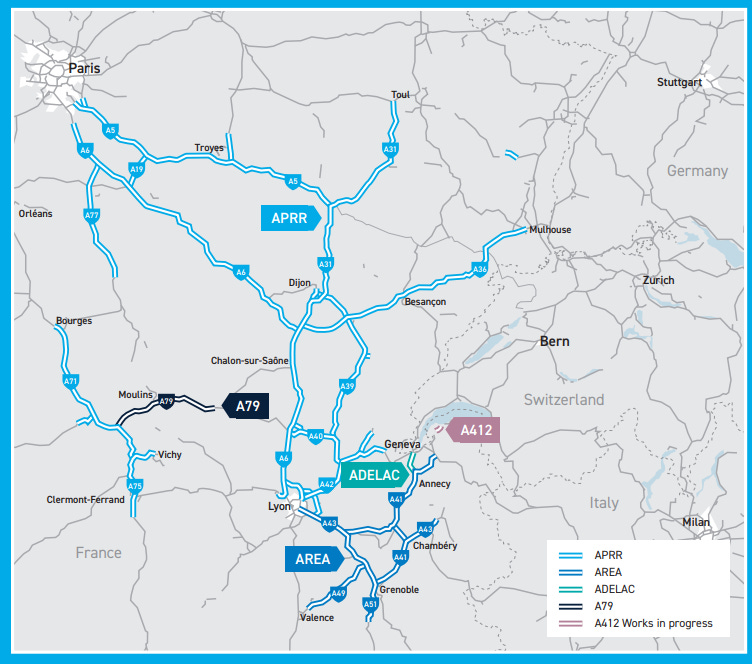

Source: Atlas Arteria February 2026 Presentation Pack

Catalysts

A primary near-term catalyst is the resolution of ongoing toll pricing disputes with the US government. As there has been a lull in price hikes, a favourable settlement would immediately increase cash generation.

In addition, in an environment of sticky inflation, ALX is well-positioned because toll increases are contractually linked to CPI. The assets act as a natural hedge, allowing revenue to keep pace with rising costs.

Competitive Moat

ALX has a wide economic moat based on physical assets not easily replicable. It is geographically and legally impossible for competitors to build parallel road networks. Furthermore, the company benefits from a long history of asset management expertise, tracing back to its Macquarie origins, with a proven ability to manage assets.

Debt & Capital Management

Toll roads are inherently capital-intensive, requiring significant Capex. ALX’s near term future will be determined by the 2035 APRR hand- back. Under the concession agreement, ALX is required to return the asset to the French government in 2035 debt-free. Consequently, investors should expect deleveraging and a change in how capital is allocated as we near the expiry date.

Risks & Sell Triggers

Volume: The primary risk is a decrease in traffic volumes due to economic downturns or structural changes in transport. If the level of volumes were to change so dramatically as to affect the level of distributions, this would be a fundamental thesis break. Luckily the volumes based on the latest annual report appear stable with some slight variations year to year.

Regulatory Risk: ALX is dependent on passing through price increases on its assets. The current risk is whether the United States government (or any government), will allow for price increases. Currently the asset is only a small proportion of revenue so the impact should be minimal but the dispute has been dragging on for nearly 3 years now.

Valuation

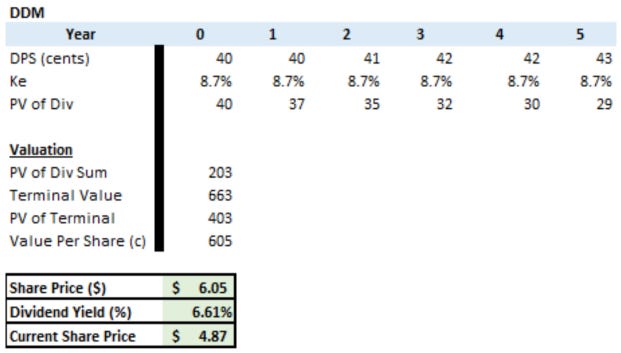

A Dividend Discount Model (DDM) was used in the valuation with a price and yield matrix to show a variety of dividend growth and terminal rate growth assumptions.

WACC was calculated as 7.6%, using a risk-free rate of 4.84% and an Equity Risk Premium of 6%. A simple CAPM model was used to calculate the cost of equity. Cost of debt was found by taking the interest expense over the debt on the balance sheet.

Using the baseline assumption of zero increases in dividend growth and terminal value, the stock appears fairly valued at $4.84 (current is $4.87). This also offer a yield of 8.3%.

Any impact from pricing increases or favourable regulatory changes will add further upside to the stock price.

Price and Yield Matrix

When adjusting the growth rates by 100 basis points from zero, we can see how the price and yield changes. Realistically a 1% increase in the dividend is reasonable, therefore a reasonable maximum share price is $5.37 (which was a previous peak in August 2025). Over the last 3-4 years, the dividend per share has been flat with no growth rate.

Positioning

Within a diversified portfolio, ALX serves as a defensive position with a low beta. Compared to Transurban (TCL) its most direct peer, ALX offers a more attractive yield and greater valuation upside. Transurban trades on a much higher valuation multiple and a lower yield as a result. Its assets are also home biased and do not offer hedged foreign income. ALX provides international exposure and can be easily traded during Australian business hours.

Disclaimer: Content is for educational purposes only and does not constitute financial advice. Always do your own research.