Market Shrugs Off Strait Tensions

Paper Mandate Market & Portfolio Commentary | 21 April 2026

Fund Status:

Bal Start: $1,069,857

Bought WTC

Sold: None

Bal End: $1,071,100

Cash: $244,446

Market Commentary

The US market was relatively flat overnight, with the SPX and NDQ only down -0.24% and -0.26% respectively. With Middle-East tensions still elevated, the Materials sector led while Communications dragged -1.41%. Breadth is returning to the market based on the equal-weight variants of the indices outperforming the standard market cap ones. Gold is still seeing support but less than before, Morgan Stanley cut its gold price target to 5,200 from 5,700/oz. One macro red flag as reported by Market Index is that the number of “S&P 500 companies lowering their forward guidance has hit the highest level since Q2 last year”. Australian futures were slightly up this morning but I’m expecting a more muted performance.

Pre-open, Hub24 (HUB) delivered record inflows and Total FUA up 22% but the stock still sold off on open. Fortunately, NWL (in the portfolio) is not experiencing any contagion effect from HUB. The session ended lower by -0.26% banking and resources weighed down the market. Financials are facing margin headwinds after trading updates. In contrast, Staples was the standout performer.

Portfolio Commentary

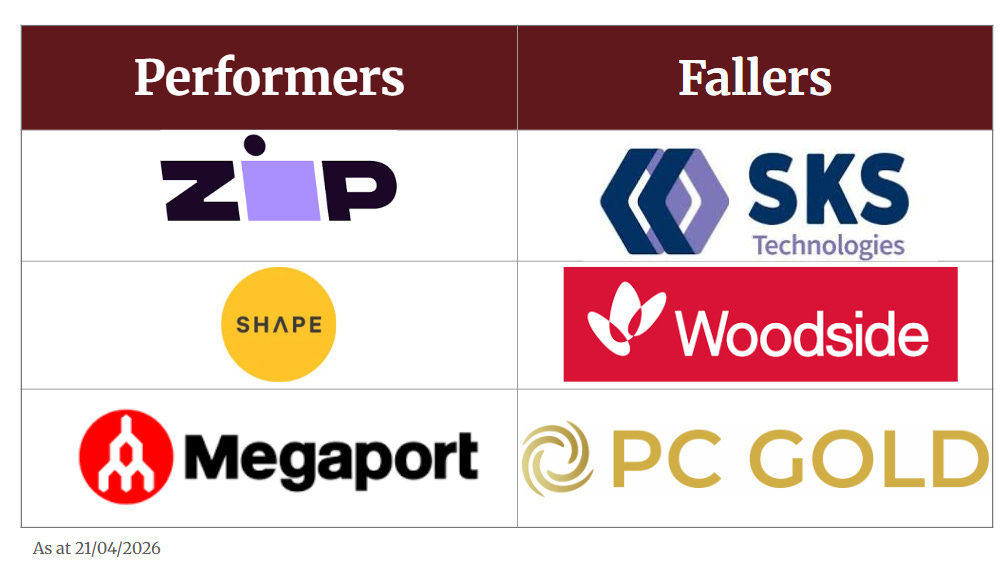

While the market had a more subdued session, the portfolio remained resistant and posted a +0.12% gain today. This was driven by ZIP, MP1, SHA, C79, and OBM; a mix of technology and materials. Pleasingly Wisetech (WTC) was also up today. Bought another 1% in the portfolio to make the weight more meaningful. One concern is the note from Bell Potter regarding global freight disruptions affecting WTC’s business. Detractors today were SKS (slight retracement from yesterday), WDS and PC2.

Investment Rationale

Disclaimer: This is a simulated portfolio. Content is for educational purposes only and does not constitute financial advice. Always do your own research.