OPEC Fractures, Oil Up & ASX 7-Day Slide

Paper Mandate Market & Portfolio Commentary | 29 April 2026

Fund Status:

Bal Start: $1,066,110

Bought None

Sold: None

Bal End: $1,066,765

Cash: $202,739

Market Commentary

Overnight, the US market retreated from record highs while European markets were up. This was a strange divergent movement. Despite the decline, Tech continued to show strength with earnings beats. Visa earnings beat estimates as consumer spending was higher. Starbucks raised its sales guidance following a strong quarterly report. However, to the surprise of everyone the UAE announced it will leave OPEC. WTI crude and Brent rallied to $100 and $111, respectively. The higher oil prices have spurred on traders in Treasury options. A Bloomberg article this morning suggested the market is expecting bond yields to rise to 5%, (lower bond prices). Going back to oil, long term the UAE exit is bearish for oil prices as now they (UAE) are unrestricted in its production. It has already indicated it intends to increase production to 6million bpd. Meanwhile the VIX moved lower, a “risk-on” signal. Gold was also lower. ASX 200 futures were down this morning ahead of a critical domestic CPI print.

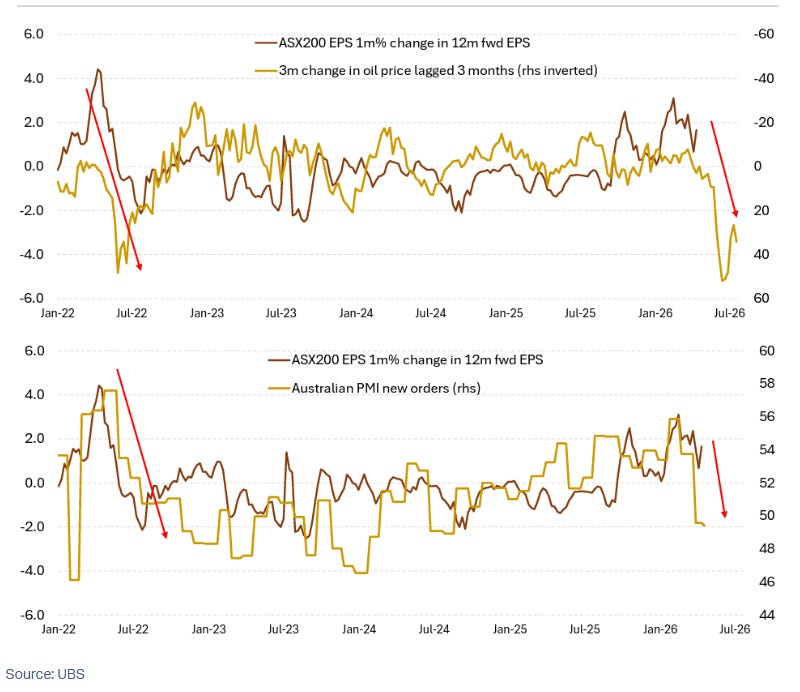

The Aussie market ended the day down, its 7th day straight. The worst performing sectors were Healthcare (-1.35%) and Financials (-0.60%) while Utilities (+2.18%) and Energy (+1.27%) were the leaders. When the CPI numbers were released, sentiment seemed to have dropped further. Persistent inflationary pressures means the market expects a hawkish response from the RBA. While energy names like Woodside rallied from the spike in oil, gold miners fell in tandem with lower prices. There was also an interesting note from UBS warning that it is still too early to “buy the dip”. They expect earnings downgrades to come through, not upgrades.

The full article is on Market Index if you are interested. Worth a read.

Portfolio Commentary

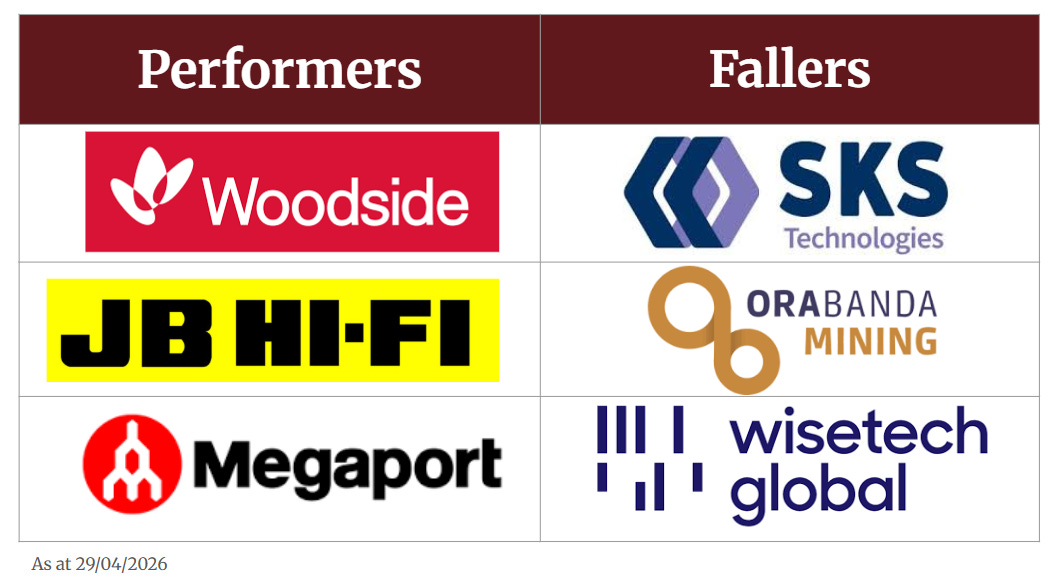

The top performer in the portfolio today was WDS (+2.0%) which released a positive Q1 update showing higher realized prices and a 96% completion of the Scarborough project. This is a gas extraction rig 375km off the coast of WA. Woodside expects to produce 8 million tonnes per annum (MTPA) of LNG from it. Photo from WDS below.

Moving to second best stock today, JBH gained (+1.8%) on no news. This one gives pause as it is a discretionary stock but seems to be resilient. MP1 was up (+1.5%) most likely from US tech strength. In other good news: 360 TP from Macquarie is $32.20 (58% implied gain). Morgans cut LOV target price to $32.50 (still 38% implied gain).

On the down side, SKS fell (-4.4%) most likely from profit taking. It did have a massive rally recently. OBM dropped (-4.1%) with the gold price. PC2 as well (-1.6%). WTC was down (-2.2%) most likely from the AI disruption trade still taking place. The market still believes AI can replace this business. A massive compliance and logistics business that provides critical software to freight companies is not (in our view) going to go bust.

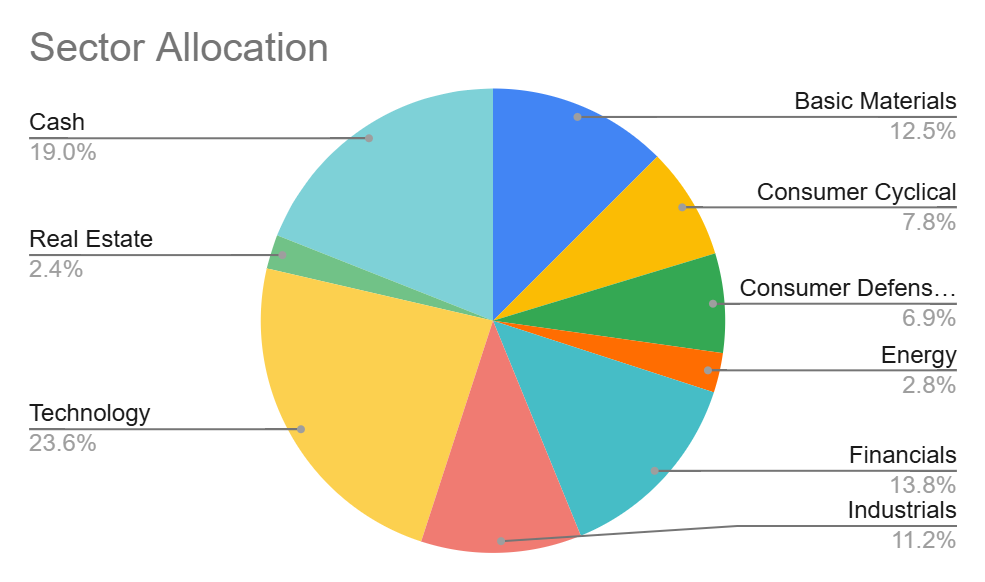

Took the opportunity to buy GDG, adding more weight to the portfolio. Based on note from UBS and the difference observed between US and AU markets, happy to hold more cash in the portfolio (~20%) for now.

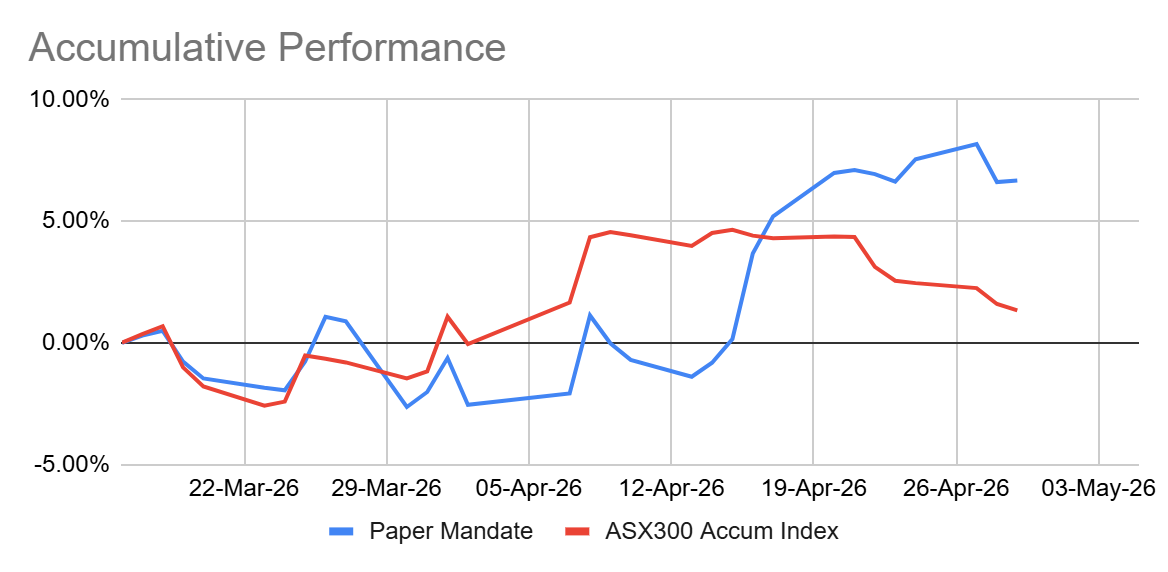

Pleasingly the portfolio was flat today (+0.06%) while our benchmark, the ASX300 Accum was down (-0.26%). The total performance of the portfolio hasn’t been shown yet. It is nearly the end of the month so why not. There will be an attribution analysis done to see what drove the returns.

Investment & Rationale

Disclaimer: This is a simulated portfolio. Content is for educational purposes only and does not constitute financial advice. Always do your own research.