PM Found Alpha in a Red April. Tech was Best.

Paper Mandate Market & Portfolio Commentary | 30 April 2026

Fund Status:

Bal Start: $1,066,765

Bought WTC, GDG

Sold: None

Bal End: $1,065,603

Cash: $181,562

Market Commentary

It was a volatile session overnight. In the mix was the Federal Reserve arguing amongst themselves (3 members objected to an easing bias commentary), big Tech earnings beat market expectations (“Yay”), and the ongoing Middle East energy crisis (“Boo”). The Fed held rates at 3.50–3.75%, some members were more hawkish. This caused 30-year Treasury yields to touch 5%. Equities had a late-session rally after earnings beats from Alphabet, Microsoft, Amazon, and Meta. It was incredible given the huge capital expenditure projections. Meanwhile Brent soared past $112 a barrel. Remember my previous post, the UAE’s exit from OPEC should place downward pressure on oil in the long term because they have unconstrained production now. But short-term is anyone’s guess. Despite the tech-driven optimism, ASX futures are down this morning.

Well, we were right, the Aussie market closed down, again. Day number 8. The Tech Index (XTX) was slightly up (0.52%) but it was actually Energy (+1.37%) and Communications (+1.32%) that were the best performers today. Some newsworthy items: Woolworths had a rough day, down over 6% after warning that fuel costs would eat into its margins. South32 dropped 8.1% following a US$1.1 billion cost blowout. Mining and gold producers were under pressure. Likely from the higher for longer interest rate risk from the RBA. Yesterday’s CPI print hasn’t helped matters. Mineral Resources was up 3% (shame we didn’t have that in the portfolio, it’s had a good run). However, WiseTech and Xero had a good day, and they are in the portfolio.

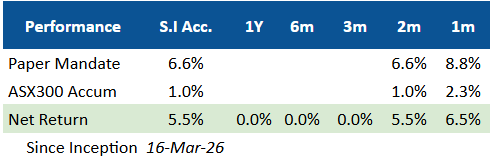

Portfolio Performance

The portfolio gained +8.8% for April. This is a fantastic result considering how volatile the month was. The benchmark (ASX 300 Accum) was only up +2.3%.

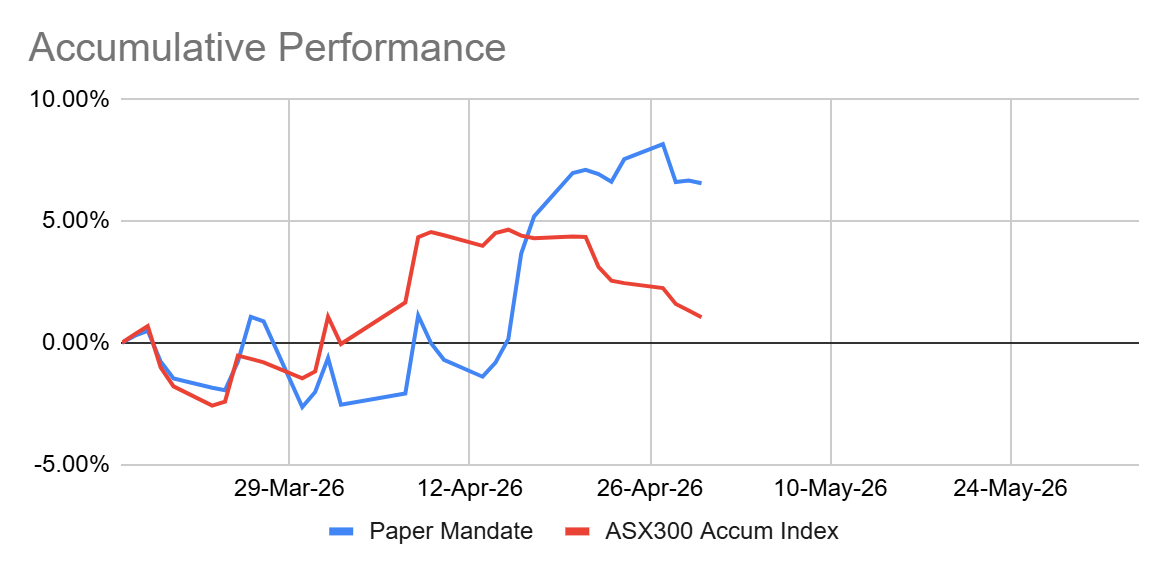

The accumulative performance is also tracking up nicely.

Over the weekend, there will be a longer, more comprehensive portfolio performance update. Showing where the returns came from and the entire portfolio to date.

Portfolio Commentary

CBO had a good rally today. Was tempted to buy more but they are nearing their previous high. So there could be profit taking activity there. CBO have elected a non-exec director, Daniel Masters, who was involved in the recent acquisition of CBO to Olive Ranch. As a reminder, AGR were involved in structuring the deal and provided funding. Masters is on the IC for AGR Partners and has now bought 11,620 units of CBO. Equivalent to $45,000 AUD at today’s price.

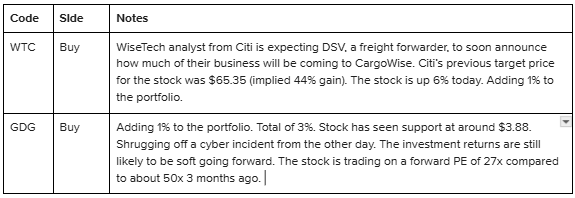

WiseTech analyst from Citi is expecting DSV, a freight forwarder, to soon announce how much of their business will be coming to CargoWise. Citi’s previous target price for the stock was $65.35 (implied 44% gain). The stock is up 6% today. Adding 1% to the portfolio.

GLF had two directors buy more units in the company. It is currently a 2.5% weight in the portfolio, and there is capacity to add more. The concern is on the RBA announcement next Tuesday. More than likely they are going to raise rates. At best keep them flat. So the real estate market is bound to suffer a fall. HMC is concerning for a similar reason.

Investment Activity

Disclaimer: This is a paper portfolio. Content is for educational purposes only and does not constitute financial advice. Always do your own research.