Structural Housing Market Tailwinds | Helia Group (ASX:HLI)

Australia LMI business with strong fundamentals and a credit tailwind

Preface

This is a historical stock analysis from February 2025. There is a stock price chart at the bottom to see how Helia has performed.

Valuation Summary

Executive Summary

Helia’s dominant market position in the LMI space and robust capital management provides a steady, predictable, return of capital to shareholders as it is also the company’s stated objective as per management.

Housing market dynamics support the LMI market despite the Australian government guarantee scheme and a decline of Helia’s policies in force.

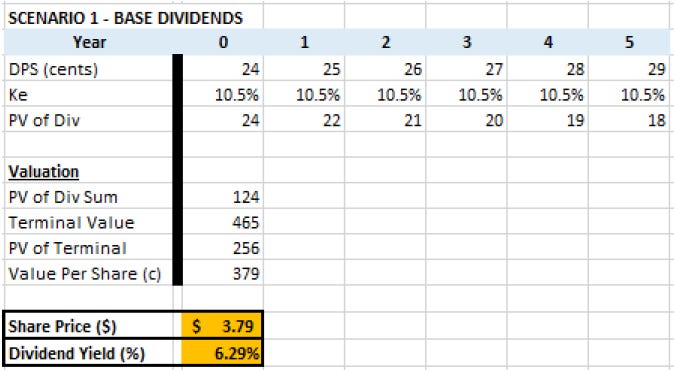

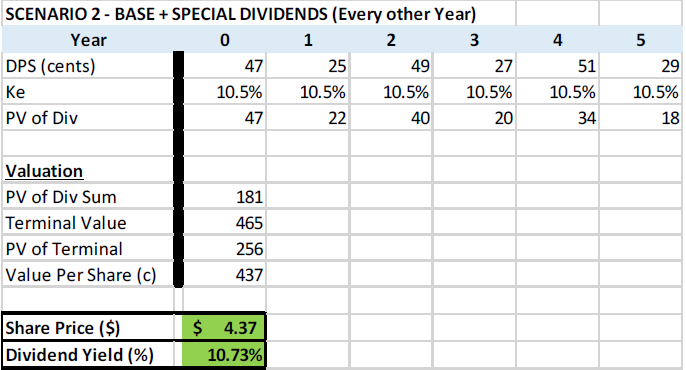

A dividend discount valuation model was employed on Helia leading a BUY recommendation, and a target price range of $3.79 – $4.37.

Helia Group (HLI) formerly Genworth Mortgage Insurance Australia Limited, is the provider of Lenders Mortgage Insurance ((LMI)) in Australia. HLI is being recommended as a BUY with a price range of $3.79 – $4.37 from its current price of $3.84 (15 February 2025). A dividend discount model was employed as Helia is seen predominantly as a dividend play.

The price range represents the lower and upper bounds based the scenario analysis that Helia pays a special dividend (upper bound) or not (lower bound). The conclusion I draw is that HLI will generate an expected yield of 6.3% without special dividends and a 10.7% yield with special dividends. With the addition of franking credits, Helia’s provides a compelling investment case.

Investment Thesis

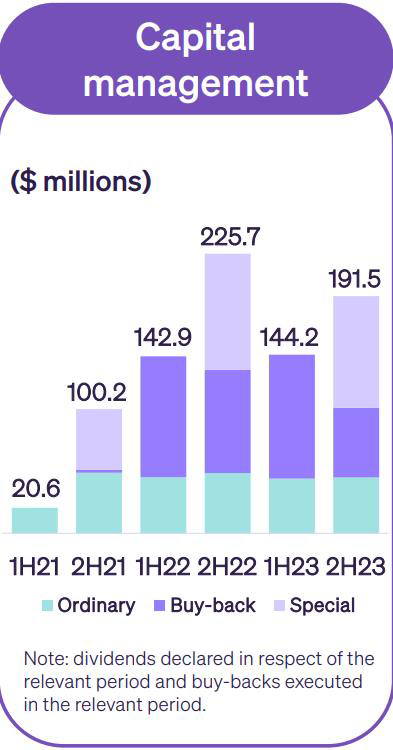

Return on Capital Policy: As per the Helia results announcement, the company targets a stable fully franked ordinary dividend and will explore options to return excess capital to shareholders through a combination of special dividends and share buybacks. Helia has consistently paid special dividends every year from 2018 and has conducted share buybacks since 2015. The outstanding number of shares have dropped at an average of 8% every year.

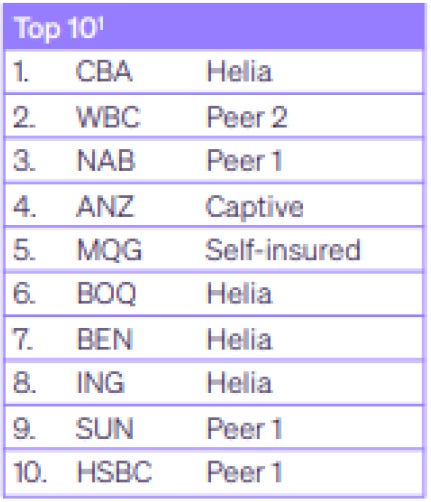

Market Position: A major lenders mortgage insurance provider to largest bank in Australia. Helia has a contract with CBA, where a 50-70% proportion of the bank’s high LVR loans are contracted to be insured by Helia. This was at 60% in FY23. It is expected to reduce to the lower end of range going forward. Helia also has a 34% market share compared to its peers.

Source: Helia 2023 Full Year Results Presentation

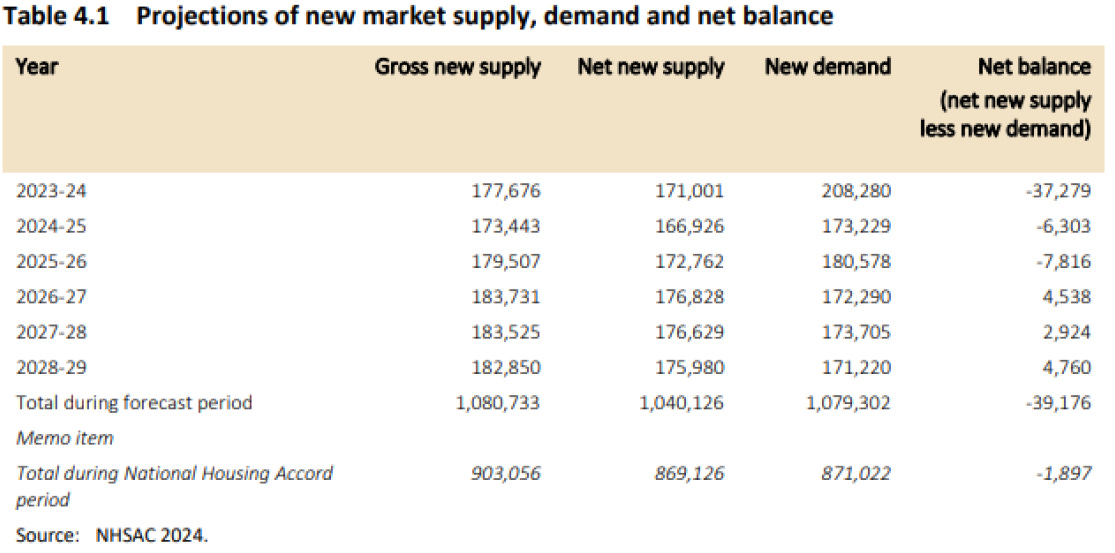

Housing Market Dynamics: The National Housing Supply and Affordability Council released a report in May 2024 that supports the housing crisis rhetoric. Stating that housing costs are nearly 20% of household income, that household savings are being eroded by inflation (savings ratio is currently less than 5%), and that Australia will be in a housing supply deficit for a number of years, with Net Dwelling Completions forecasted to be below New Demand until 2026-2027. This supports the thesis that Lenders Mortgage Insurance will a) still be needed despite government support, and b) the value of dwellings under insurance will continue to increase.

Source: National Housing Supply and Affordability Council - https://nhsac.gov.au/sites/nhsac.gov.au/files/2024-05/state-of-the-housing-system-2024.pdf

Business Segments

Insurance Book

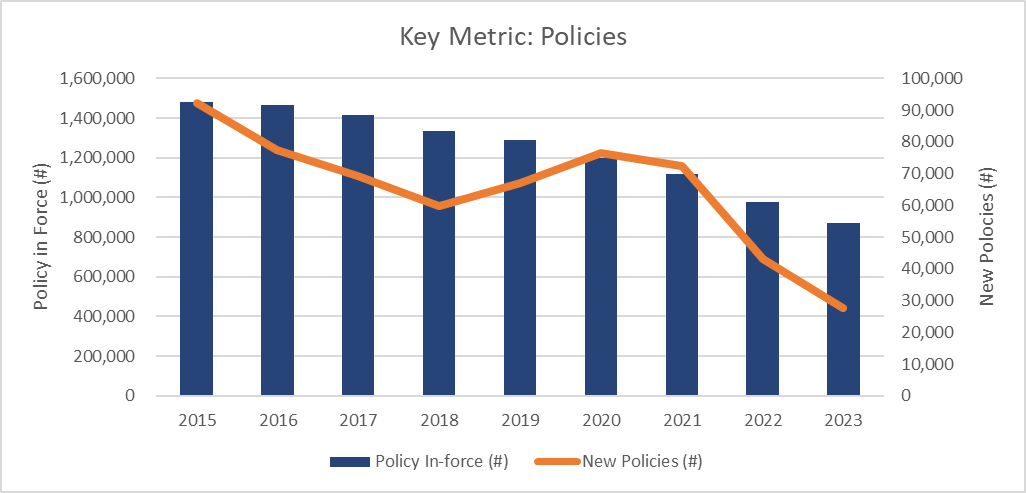

On a cursory review of Helia’s annual reports, one can be forgiven in thinking it is a declining business. However, the data shows that the value of Helia’s insurance book per policy is increasing. Leading to an increase in net premium revenue and net profit after tax.

One key insight I gleaned through reviewing the data was that the number of policies in force have been in decline and the number of new policies also continue to decline.

Source: Helia annual reports 2015 to 2023 – calculation by author

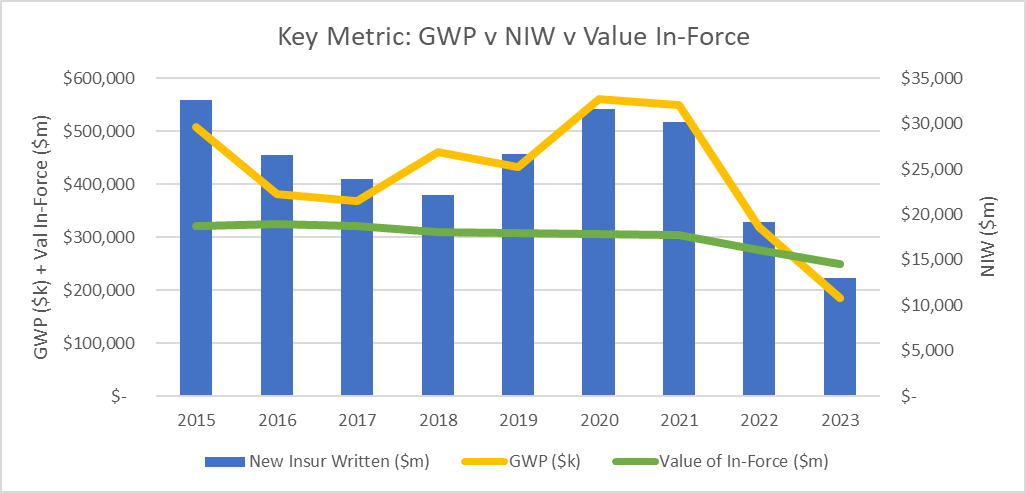

As a result, the value of all policies in force has been on a slow but steady decline. In addition, Gross Written Premiums ((GWP)) and New Insurance Written ((NIW)) have also been in decline. This all sounds like a bad news story.

Source: Helia annual reports 2015 to 2023– calculation by author

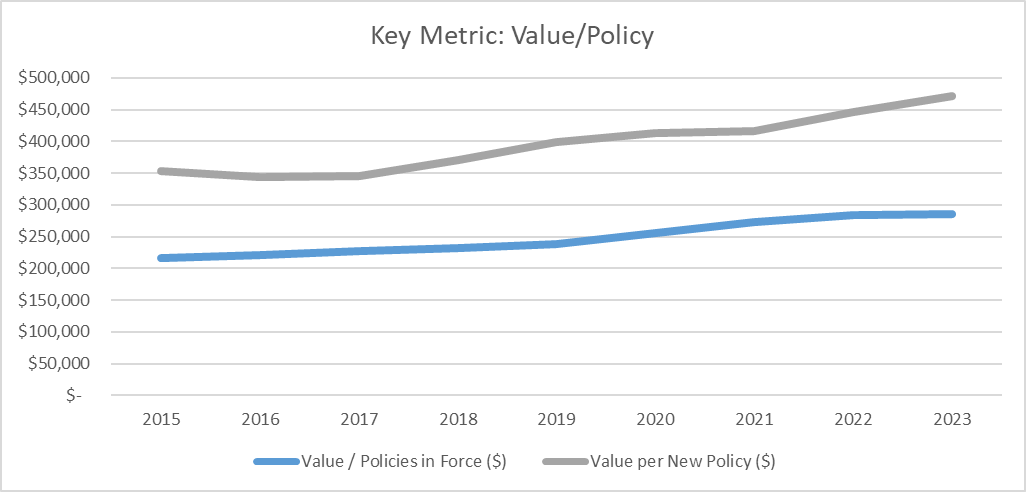

However, the value of policies has been increasing overtime, partly confirming the housing market dynamic thesis – less supply leading to higher house prices leading to higher insurance values. We can see that Helia’s Value per Policy In-Force and the Value per New Policy are both in steady incline.

Source: Helia annual reports 2015 to 2023– calculation by author

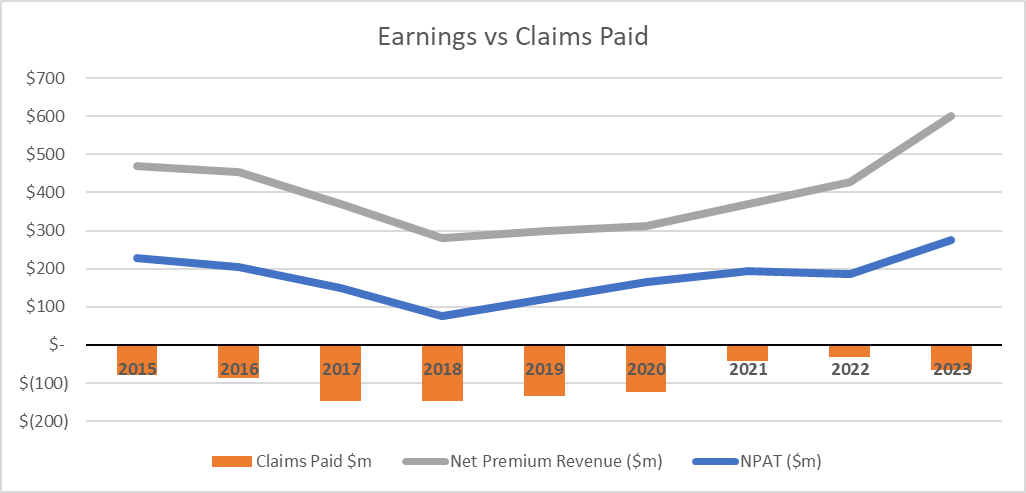

As house prices rise, the value of each insurance policy increases. This should hit Helia’s bottom line, generating higher earnings as older, lower value, policies mature and newer, higher value, policies become the majority of Helia’s insurance book. We can see that Net Premium Revenue and ((NPAT)) have turned a corner and are now higher than they have been since 2015.

Source: Helia annual reports 2015 to 2023– calculation by author

Investment Book

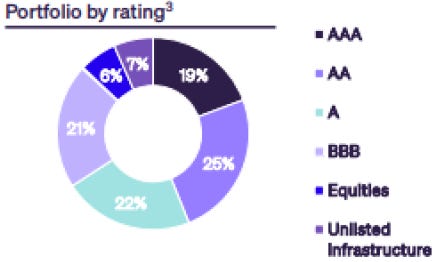

Helia’s investment portfolio is predominantly in fixed income assets, constructed to match the cashflows and duration of the expected claims in the insurance book. Investment income in FY23 ($173m) was significantly higher than FY22 (-$81m) pcp due to higher interest, higher dividend income, and mark-to-market investment gains. This is most likely a once off due to the current fixed income environment benefitting and narrowing spreads.

The duration of the fixed income assets is 3.7 years with 66% of the portfolio in investment grades AAA to A. A smaller proportion of the investment portfolio is in Equities, Unlisted Infrastructure, and Derivatives. Overall, the investment book appears well managed and diversified.

Source: Helia Investor Presentation FY23

Seeking Alpha Article

A historical article found on Seeking Alpha indicates Helia Group is a Buy. This analysis was conducted prior to Genworth selling its stake. The article states that Helia’s business is correlated to the mining sector in Australia, citing that Western Australia housing price decline as the reason for the drop in stock price.

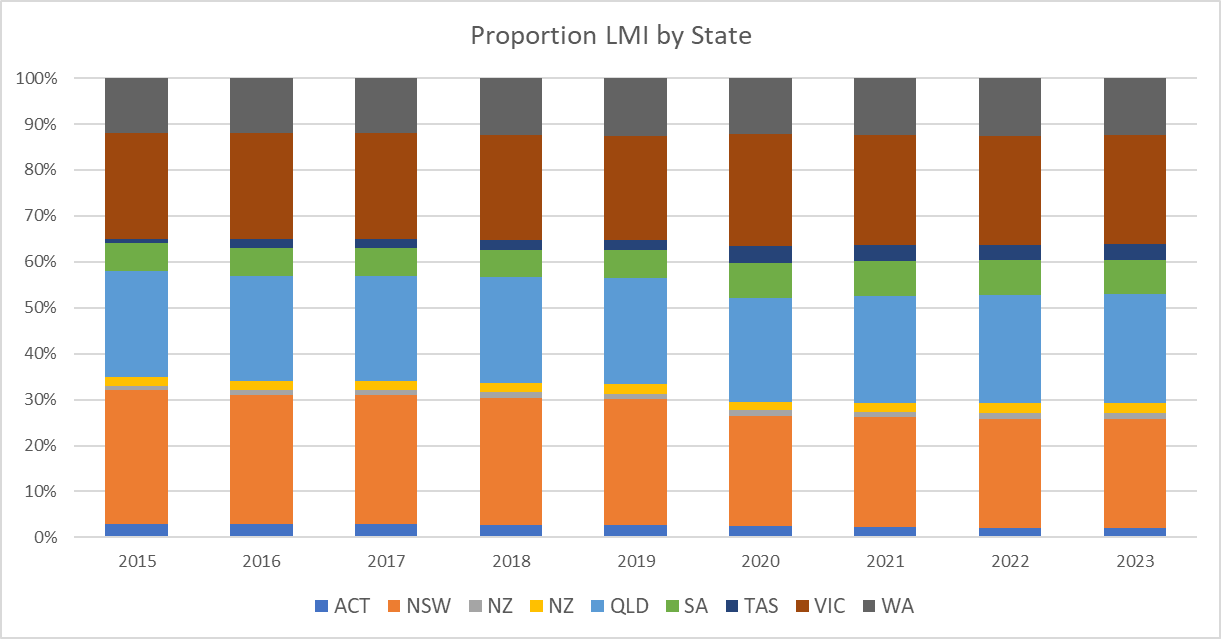

I do not agree with this assertation as Australia is more than just mining. In addition, only 12% of the Helia’s insurance book is located in Western Australia. This has been the case historically

Source: Helia annual reports 2015 to 2023 – calculation by author

Competitive Moat

According to Morningstar, Helia does not have a competitive moat. However, given that Helia is the largest player in a competitive and concentrated market for lenders mortgage insurance, I think a narrow moat is warranted. It has a contract with the largest bank, CBA, whom renewed its contract in 2022, for three years.

Given that CBA is 60% of Helia’s insurance book, this does constitute a risk for Helia – should CBA decide to not renew their contract. However, APRA regulates the market, and I doubt the regulator would allow a competitor to monopolise the LMI contracts of the major banks.

Arch Capital Group is a new entrant to the Australia market and acquired Westpac’s LMI business. Arch provides insurance, and reinsurance globally. However, market participants are cautious of Arch’s commitment to Australia long term, based on commentary and market rhetoric.

Company Management

Helia’s board of 8 members has an equal split of men and women. Pleasingly all the directors are listed as independent, including the Chair. Pauline Blight-Johnston is the CEO of Managing Director of Helia. She joined in March 2020. Prior to Helia, she worked at Challenger, AMP and RGA Reinsurance, so has ample experience. Blight-Johnston has been four years in the role and has maintained consistent return of capital to investors. Unfortunately, NAB did not renew their contract with Helia (November 2020) under her tenure but that may have been an outcome out of her control.

The executive team is also a mix of men and women, all of whom appear to have significant experience in the industry despite some of the shorter tenures. Remuneration STI’s and LTI’s are scored against specific goals that the board members need to meet for bonuses. In addition, halve the remuneration of the executive team (51% on average) is deemed “at risk and performance based” or deferred, and is based on achieving company goals. This provides a great alignment with shareholders.

Debt & Capital Management

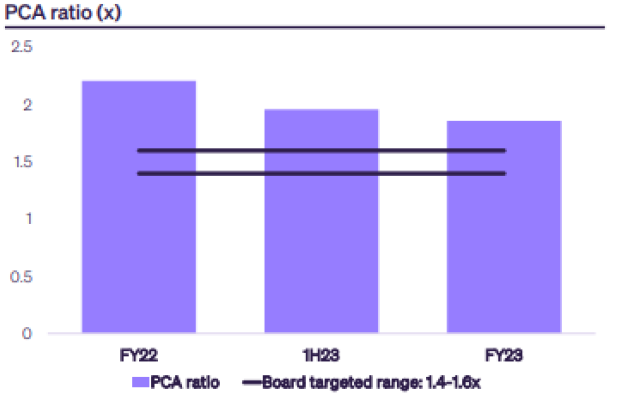

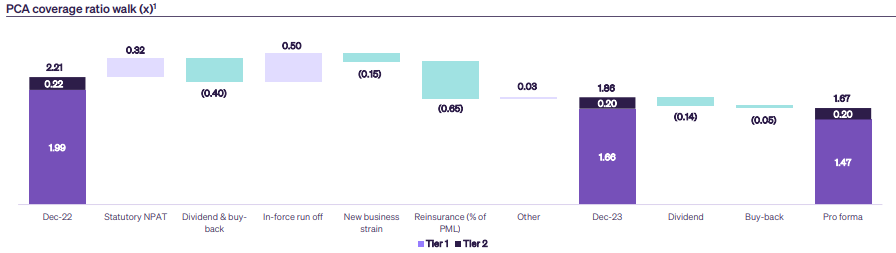

Helia is required to hold regulatory capital and has a board targeted Prescribed Capital Amount coverage ratio of 1.4-1.6x. The current ratio sits at 1.86x, representing $247m above the target range. The ratio has reduced from FY22 to FY23 due to low new business and lower reinsurance.

Source: Helia Investor Presentation FY23

Most of the capital base is Tier 1

Source: Helia Investor Presentation FY23

While the regulatory capital requirements are burdensome, I’m encourage by how well Helia manages the capital requirements, while paying regular dividends, and conducting regular share buybacks.

Risks & Sell Triggers

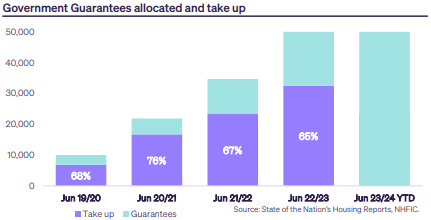

Government Guarantee Scheme – The First Home Guarantee (FHBG) reduces the need for LMI. Under the FHBG, an eligible buyer can buy a home with a 5% deposit without paying Lenders Mortgage Insurance. From 1 July 2023 – 30 June 2024, 35,000 FHBG places are available. The take-up of this scheme is roughly 65%. If this offering were to expand as part of a Federal Government initiative, this would sorely reduce the Total Addressable Market for Helia.

Source: Helia 2023 Full Year Results Presentation, Housing Australia

Loss of Major Contract – If CBA does not decide to renew their contract with Helia in 2025, this will be a material loss for the business. At that point the investment thesis no longer holds and I would recommend selling the stock. In addition, there are other avenues that the banks can take in order to not use Helia for LMI. For example, they could choose to have the credit risk on their book or not lend higher LVR loans. As of now, Helia have given guidance of $360m-$440m for FY24

Housing Market changes – Should the current housing market dynamics change dramatically; this would materially affect Helia. If houses were to become significantly cheaper due to oversupply, or should the banks decide to no longer lend on higher LVRs, or if claims spiked beyond what Helia could reasonably handle, any would be a thesis break and warrant a sell of the stock.

Valuation

A valuation was conducted using a Dividend Discount Model under two scenarios; 1) the baseline level of dividends (no specials) and 2) a dividend scenario that includes special dividends every other year.

WACC was calculated as 9.9%, using a risk-free rate of 4.05% and an Equity Risk Premium of 6%. The dividend growth rates were assumed to be 4%. A Cost of Equity of 10.5% was used as the discounting rate

Scenario One: Ordinary dividends of 24 cents per share increasing at 4% per year. At a valuation price of $3.79, this equates to a dividend yield of 6.29%. Ordinary dividends are 100% franked so the yield figure may be higher depending on person tax circumstances.

Scenario Two: Using the same baseline level of dividends as per Scenario One (24 cents per share increasing at 4% per year) with the addition of a special dividend of 23 cents per share, every second year. This was found by averaging the special dividend given to shareholders over many years. At a valuation price of $4.37, this equates to a dividend yield of 10.73%. While ordinary dividends are 100% franked, special dividends are not. Final yield figures may differ depending on person tax circumstances.

Positioning

Helia provides a steady a consistent return of capital to shareholders via dividends and buybacks. The value of policies in the insurance book are increasing while the number of policies is decreasing. This muddies the assessment of the insurance book in the short term. However, current housing market dynamics are in favour of the LMI business, as the lack of housing supply pushes up prices, forcing buyers to purchase LMI. For investors, Helia provides a decent income producing stock for the short to medium term, recommended as a BUY with a target share price range of $3.79 – $4.37, for a 6.3%-10.7% dividend yield respectively.

April 2026 Update

Since the initial analysis in Feb 2025, we can see the stock price has been significantly higher than predicted. The upper bound in the analysis was $4.37 while the actual price has waxed and waned well above.

Due to the housing crisis in Australia, sales values have increased along with the revenue stream of Helia. The size of the dividend payouts increased since February 2025. The yield at the current share price ($5.44 as at 10 April 2026) is roughly 15% using the last 12 month of dividends (less the special in March 2026).

This was significantly beyond the expectations set in the analysis. Investors here had higher dividend payments plus capital appreciation. A good outcome.

Disclaimer: Content is for educational purposes only and does not constitute financial advice. Always do your own research.